The need for hot water in Australian homes has changed a lot over the last decade. Showers are longer. Appliances […]

If you’ve been longing to upgrade your home’s energy efficiency but held back by the upfront cost, this could be your moment.

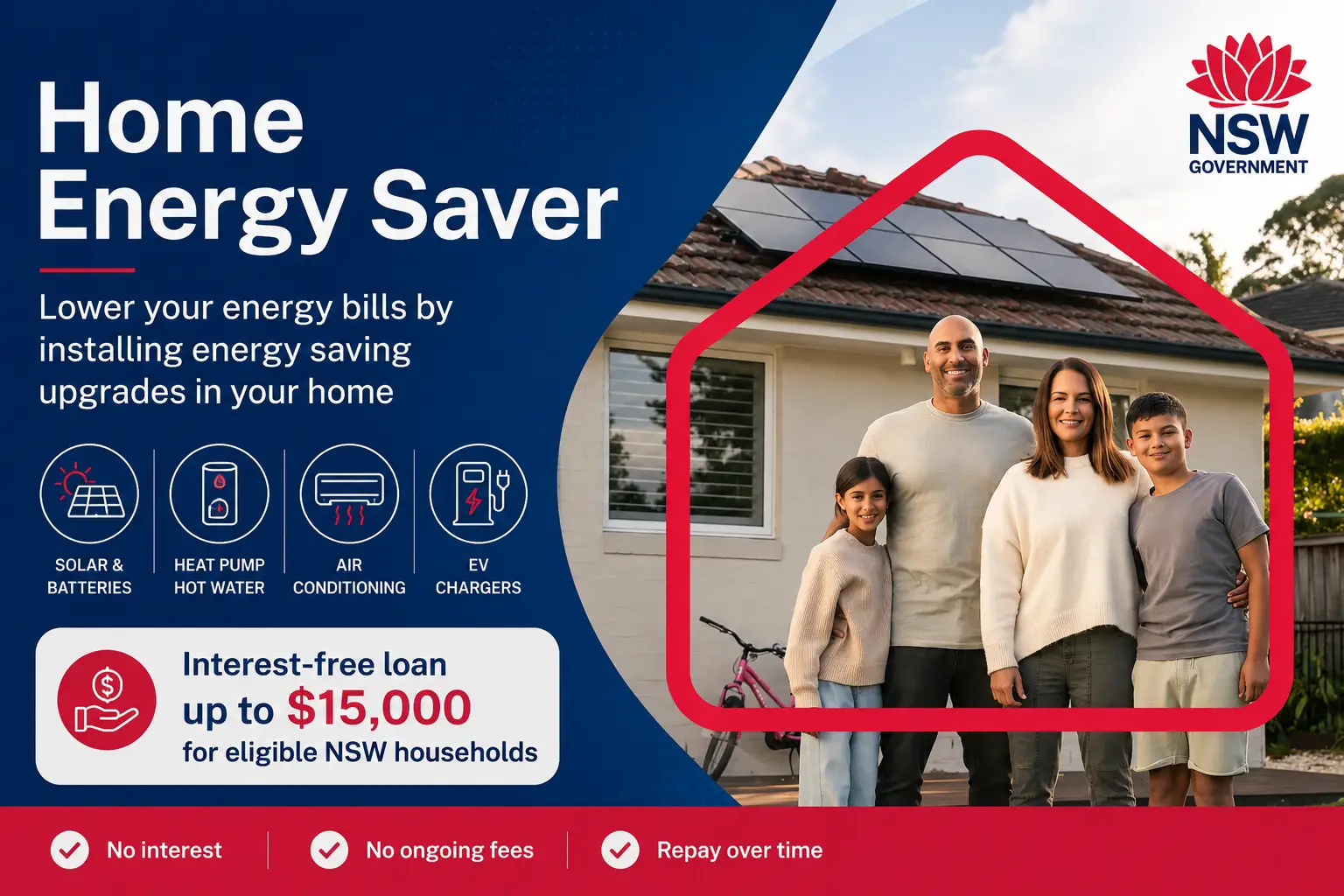

The NSW Government has introduced a Home Energy Saver Program offering eligible households interest-free loans of up to $15,000 for approved energy upgrades.

This means you can now install solar panels, add a battery, upgrade insulation, replace an old hot water system, or switch to more efficient heating and cooling without paying the full cost upfront.

Instead, you’ll spread the cost into manageable repayments and start reducing your energy bills sooner.

Here’s how the NSW Home Energy Saver Loan works, who can apply, and which upgrades deliver the biggest savings.

The NSW Home Energy Saver Loan is a state government program that offers zero-interest, fee-free loans up to $15,000 to help you lower your electricity bills. It is the core part of the NSW Government’s $557 million Home Energy Saver Program.

The loan is designed to solve one main problem: the high upfront cost of clean energy. While most people know that installing things like solar panels, home batteries, heat pumps, or ceiling insulation will significantly cut their power bills, actually buying this equipment requires thousands of dollars in cash that many families simply do not have readily available to spend.

This program removes that entry barrier completely. It acts as a bridge, giving eligible homeowners and landlords the money to fully pay for modern energy-saving upgrades today, allowing you to pay it back smoothly over time instead of all at once.

The NSW interest-free energy loan operates under a strictly regulated, consumer-first framework that eliminates these hidden traps entirely.

Strict Exclusions: This program cannot be utilised for properties categorised as social housing, community housing, or commercial short-stay holiday accommodations (such as Airbnb properties). Renters are explicitly ineligible for the loan element itself, as financing must attach structurally to a property owner’s profile, though they can access upcoming discount modules.

The NSW energy efficiency loan is highly flexible, allowing property owners to mix, match, and bundle diverse energy technologies into a unified installation schedule up to the $15,000 ceiling.

The program offers the following to support home upgrades:

Since you have 10 full years to pay off the interest-free home energy upgrade loan, your regular monthly or fortnightly payments are split into tiny, easily affordable amounts. At the same time, your new energy-efficient upgrades instantly slash your electricity costs. Because the amount of money you save on your power bill is bigger than the small amount you pay toward the loan, you are left with extra money in your bank account right away.

For example;

If your new system saves you $150 a month on electricity but your loan repayment is only $80 a month, you are instantly $70 ahead each month. Instead of having to find extra money to pay for the equipment, the upgrade actually drops your overall living costs from your very first billing cycle.

The Home Energy Saver Program divides support based on whether you own, rent, or lease out the property:

Navigating the NSW Home Energy Saver Loan application process is straightforward when executed through authorised channels. Follow this precise blueprint on how to apply for the NSW Home Energy Saver Program successfully:

Review your financial records to ensure your combined household taxable income sits beneath the $210,000 baseline. Collect your recent property council rates notice and individual ATO notices of assessment to verify your identity and ownership profile.

The state does not process loan applications directly through government departments. Instead, choose between the two accredited fintech administrators: Brighte or Plenti. Both companies feature dedicated digital portals tailored exclusively to this state-backed program.

Use the provider’s specialised directory to find an installer holding active NETCC (New Energy Tech Consumer Code) credentials. Only tradespeople registered within these strict regulatory frameworks can upload applications into the state system.

Have your selected vendor complete a physical or digital site analysis of your switchboard, roof condition, and thermal footprint. The vendor will formulate an itemised quote. Under strict program rules, this quote must explicitly display all component warranties and deduct any existing federal or state rebates (such as federal STCs or state-level certificates) before arriving at the final loan balance.

Once you accept the quote, the contractor triggers an automated referral link via Brighte or Plenti directly to your email or smartphone. Click the secure link, fill out the basic credit assessment details, upload your income verification documents, and submit. Approval notifications are typically processed within minutes via automated digital underwriting.

The accredited contractor coordinates an installation date to deploy the hardware at your property. Once the physical work is complete, you will inspect the system and sign a digital completion certificate. The finance partner then pays the installer in full, and your zero-interest repayment schedule commences.

To roll out the program seamlessly across the state, the NSW Government partners with two elite leaders in the Australian green finance landscape:

Widely recognised for administering large-scale clean energy financing programs for the ACT and Tasmanian governments, Brighte brings exceptional operational experience to the Home Energy Saver NSW rollout. Their robust vendor marketplace connects applicants with highly rated, thoroughly vetted local solar and insulation specialists, ensuring zero upfront friction.

Plenti is a premium ASX-listed financial services provider renowned for fast digital processing and flexible lending terms. Plenti’s consumer portal gives applicants clear visibility over their principal balances, providing robust consumer protection mechanisms and automated bank-feed verifications to keep the application process rapid and transparent.

Both lenders are legally bound by strict responsible lending laws under their respective Australian Credit Licences (ACL), ensuring all credit products are clearly communicated and safe for consumers.

The zero-interest loan coordinates with several prominent frameworks as follows:

Yes. The program is specifically built to complement existing environmental incentives rather than replace them. The state architecture requires all installers to stack available federal and state rebates upfront, effectively reducing the principal amount you need to borrow.

| Incentive Scheme | Operational Mechanism | How It Integrates With Your Loan |

| Small-scale Renewable Energy Scheme (SRES) | Federal STC point-of-sale discounts on solar panels. | Automatically deducted from the quote by your installer before calculating the remaining balance for the loan. |

| Energy Savings Scheme (ESS) | State incentives for high-efficiency commercial/residential equipment. | Applies directly to hot water heat pump and air conditioning replacements to push hardware costs down. |

| Peak Demand Reduction Scheme (PDRS) | Credits targeted at home battery storage installations. | Directly lowers the financial barrier when applying for a $15,000 loan for home batteries in NSW. |

Later in 2026, the NSW Government will introduce a separate $77 million targeted discount pool providing upfront cash subsidies of up to $4,000 for lower-income households (earning under $80,000 annually) or concession card holders.

If your household falls into this bracket, the strategic sequence is critical: you are strongly advised to apply for the cash subsidy first. Once the $4,000 discount is deducted from your system price, you can use the NSW government loan for home energy upgrades to finance the remaining balance completely interest-free. This stacked approach can drop the self-funding payback period of a premium solar and battery setup to under four years.

To maximise the impact of your $15,000 allocation, it helps to understand which technological combinations yield the highest financial returns relative to their installation costs.

Deploying a zero-interest solar loan NSW 2026 configuration is the most effective way to eliminate power bills. While solar panels wipe out your daytime running costs, adding a battery ensures you remain insulated from high peak-tariff rates (typically levied between 5:00 PM and 9:00 PM). By storing afternoon solar power and running your home off battery power at night, you can slash your grid reliance by up to 80-90%.

Water heating represents roughly 25% of the average Australian household’s total energy footprint. Conventional electric hot water tanks act as large, inefficient resistive heating elements. By switching to a modern heat pump, the system extracts ambient warmth from the surrounding air to heat your water supply. This process uses up to 75% less electricity and can be easily programmed to run entirely during peak solar generation hours.

Introducing high-grade interest-free financing for insulation in NSW addresses the root cause of high utility bills. If a building features poor thermal resistance, your climate systems must work overtime to maintain comfortable indoor temperatures. Upgrading your ceiling insulation to a high R-value traps conditioned air inside, lowering your heating and cooling expenses by up to 30% completely passively.

If you intend to hold your property for the foreseeable future, the program is highly worth it. Under standard commercial green finance terms, borrowing $15,000 over 10 years at an average 7.5% interest rate would cost you roughly $6,400 in interest alone.

By completely eliminating that interest overhead, the state ensures that 100% of the utility savings generated by your new equipment flow directly back into your household budget from day one.

You are effectively taking money that would have been spent on ever-increasing power bills and redirecting it into an asset that builds long-term equity in your home. It provides an ironclad defence against cost-of-living challenges while contributing directly to a cleaner, more resilient state grid.

It is an interest-free loan that must be fully repaid over an agreed term of up to 10 years. It is not a free grant or an unconditional handout, though it features zero interest and zero ongoing fees.

Yes. If you already have a functional solar array, you can use the NSW zero-interest loan for solar pathway to install a companion battery storage bank, complete a comprehensive switchboard upgrade, add high-quality ceiling insulation, or replace your old gas cooktop with an induction model.

No. Because the loan requires structural hardware modifications to the property title, the loan is strictly reserved for owner-occupiers and landlords. However, renters will be eligible to access the upcoming targeted energy discounts later in 2026, provided they obtain documented permission from their landlord.

If you sell the property, the outstanding balance of your loan must be fully settled at the point of property transfer, typically using proceeds from the sale during settlement, as the loan cannot be transferred to the new buyer.

Visit the official NSW Government Home Energy Saver gateway at energy.nsw.gov.au/home-energy-saver to confirm your property’s eligibility and access the authorised Brighte and Plenti vendor directories.

To keep your debt as small as possible. By law, installers must apply federal and state discounts to your quote first. This ensures you only borrow the remaining balance, keeping your loan amount small and your monthly repayments at an absolute minimum. It also preserves the government’s budget, so it can help more households.

You are fully protected by the Australian Consumer Law. Because the program requires all installers to be NETCC-accredited, your hardware features strict product warranties.

The need for hot water in Australian homes has changed a lot over the last decade. Showers are longer. Appliances […]

Hot water systems rarely get attention until they fail or the power bill arrives. Yet in many Australian homes, water […]

You don’t really think about your hot water system until it stops. Then suddenly everyone’s talking about it. The shower […]